Student loans for everyone

How to help young people after Covid

After Covid, people might want to “give back” to young people who’ve given up a year or more of the best part of their lives to help suppress a disease that poses only a very small danger to them. That’s not really how I see it - I think most younger people do not want older loved ones dying of Covid, so even if they are not the main beneficiaries of lockdown policies, they benefit from them as well. But if that’s the way things go, one option worth considering may be to let young school-leavers access loans on student loan terms for purposes other than going to higher education.

How income-contingent loans work

In England we give income-contingent loans to allow people to pay for university fees and living costs. This means they don’t pay those loans back unless they earn above a certain income (currently £25,716/year), above which they pay 9% of their earnings in repayments. The loan incurs an annual interest rate equal to an annual measure of inflation plus 3%. Once you have paid off the loan, no more repayments are taken, and any amount still unpaid thirty years after the loan was first taken out is written off.

This is very generous. Under a less generous repayment scheme that was in place until recently, with a lower income threshold for repayment, out of every £1 borrowed by students the long-run cost to the government was 43.3p. That means that there is a de facto subsidy to university education, which may lead to more people going to university than would choose to do so if the system was neutral. That might be reasonable, if university education has positive externalities, or it might be inefficient if it doesn’t, or if it has negative externalities.

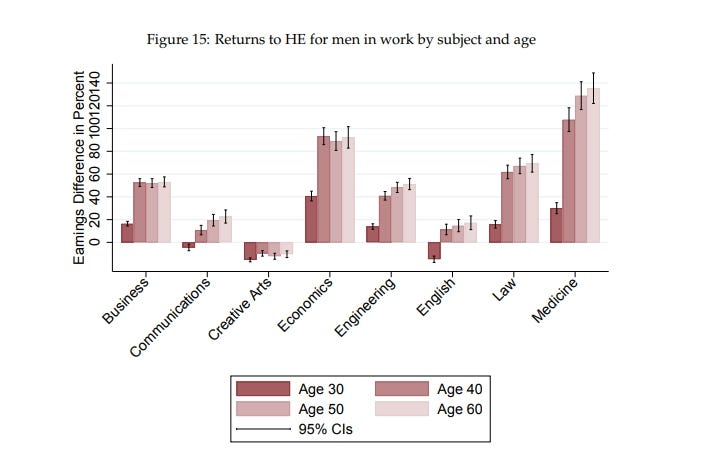

One negative externality may be the “arms race” that occurs as more and more people get university degrees. Since part of the value of a university education is demonstrating your talents to future employers (eg, it is hard to get a good degree at a good university without being pretty smart), having more people with university education interferes with this signal. This means people have to compete more intensely for the top places (eg, at Oxford or Cambridge) or go into graduate education that may not be the best use of their time and money.

From a tender age all pupils (and their parents) are fixated on the eight-hour multiple-choice entrance exam for university, to which three-quarters of school-leavers go. Because competition is fierce, parents plough money into private tuition—over 18 trillion won ($15 billion) last year, or more than a tenth of household spending—to improve their children’s chances of getting into the best secondary schools (see chart).

This has led to intense competition even for places in crammers. The most desirable hagwon set their own entrance exams and refuse applicants with a low score. Some of those rejected reapply several times. Hence a new breed of cram schools has emerged that mostly coach students to get into more illustrious ones. They are called sekki (“cub”) hagwon.

It’s not obvious to me that university education has positive net external effects, especially at the margin. Having some graduates is probably good for society, but diminishing returns surely set in at some point, and it’s quite possible that the bad outweighs the good. If more university education is not unambiguously good for society as a whole, creating a big bias in favour of it seems like a bad idea.

It is important to differentiate between this subsidy and the income-contingent element of the loan. The subsidy - the amount that, overall, is never repaid by any student - is what society contributes to give people an incentive to study at university. But the fact that the scheme is income-contingent also means that graduates are subsidising each other. This shares the risks of doing a degree between graduates - doing a degree may give you a chance of having a high-paying career, but a certainty of taking on debt, which may discourage people who are (rationally) loss averse. Making the loan income-contingent means the debt is also dependent on your career success.

Ending the pro-university loans bias

My proposal is to eliminate the bias in favour of university education by allowing any school leaver to access a loan on the same terms as the student loan scheme. This would mean that, in practice, you could borrow £27,000 or more at the age of 18 to spend on whatever you wanted, to be repaid as you started earning more as you got older on the same terms as university loans are repaid

This would give a similar degree of freedom and subsidy to every young person that is currently only available to young people who are somewhat academically gifted, and who choose to use those gifts by going to university. In some parts of the country, where very few people go to university, the policy would mean a major cash transfer that currently only goes to universities and university towns, helping with the government’s aim of ‘levelling up’.

This would allow them to spend the money on things that will genuinely help their lifetime earnings that do not qualify for student loan support right now. A lot of programmers now learn their trade by doing boot camp courses that only take a few months. Apprentices currently earn very little (which is fine, it makes it possible for more places to take them on), so they could use these loans to afford to live where the apprenticeship is, making apprenticeships a more viable option for many people.

The government is moving towards this kind of approach, but by being too timid about letting people decide how to spend the money themselves, it will inevitably involve bureaucracy and box-ticking, and miss out on new innovations in self-improvement that a government agency has not yet approved.

Others will likely use the money to get set up in life: using it as a deposit on a home, buying a car, or moving somewhere with better job opportunities than their hometowns. In many parts of the country, owning a car is absolutely vital to access a bigger job market than your immediate surroundings offers.

Probably a lot of people would spend some (or a lot!) of the money on holidays, boozing and socialising. That’s fine - fun is a significant part of many students’ university experience, and is a good reason to go to university. If the loan allowed people to have more fun without going to university, it would give more people access to one of the key parts of a university education without the time and cost of doing a university degree. It seems bizarre to say that only studious young people should have the ability to get drunk and party on a Wednesday night, but that is what the current system entails.

What this would mean for university students

The best argument against my proposal is that it ends much of the risk-sharing element of the loan. But since the same loan terms are currently offered to students who study medicine or economics as study English or the creative arts, which have wildly different expected returns in terms of lifetime earnings, I question whether this element is really very strong in our current system. Making the money freely available to everyone might actually allow a true risk-sharing mechanism to emerge for those who do go to university (which would likely offer different terms according to subject and institution).

Ending the university bias does not need to involve ending the subsidy for university education. It can also be done by giving the same subsidy to whatever alternatives people would like to choose instead. If the consequence of this is fewer graduates, and perhaps fewer universities, so be it. No institution has the right to exist at the public’s expense if it is not providing value to the people it serves - if, once the bias was eliminated, some universities could not give students an offer that was worth it without a major subsidy in its favour, they should shut down.

Pressures like that may force universities to offer better value for money, too - cheaper courses, since students would have more alternative options and could use the remainder of their loans on other things, and a greater focus on improving long-term outcomes for their graduates. It would finally force universities to compete - not just with each other, but with the rest of life’s opportunities too.

Anti-Virus: the Covid FAQ

Along with friends, I’ve put together a site that tries to respond to some misinformation and dodgy claims made about Covid. It also catalogues some of the claims made by some of the most prominent “lockdown sceptics” and “Covid sceptics” (eg, people who claim that there is no pandemic, there are just a lot of false positive Covid tests). It’s called Anti-Virus, and it’ll be updated regularly throughout the pandemic.

I’ve also written about the eight biggest Covid myths, based on that site, for the New Statesman, which you can read here.