How I save money

How I save and invest money, do my monthly budgeting, and why I don't plan to buy a house

My last issue focused on how to spend money wisely. In this issue I want to outline how I save my money and why I do it that way. This is not investment advice, I am not qualified to give advice, I am just telling you what I do.

Every month when I get paid, I use Monzo pots to divide my income between bills, savings, and normal spending for the month. For those who use a bank with “pots” (which are little sub-accounts for dividing money between), I’ve outlined my budgeting method at the end.

How I manage my savings

I try to keep only a small amount of money in cash – a bit more than a month’s worth of expenses (including rent). I don’t keep months in cash as an “emergency fund”, as some advise: in a downturn, even a major one, I can sell investments to cover my emergency expenses, and in my view the cost of drawing down investments in a downturn is less than the cost of keeping a large sum of money in cash over time, as this post argues.

To me, keeping savings in cash is like setting fire to it. It earns so little interest that inflation means it is eaten away bit by bit every day. Consumer price inflation in the UK has averaged 1.9% since 2010, meaning that £1,000 kept in cash from 2010 would have lost about £180 in purchasing power by now. Cash savings could also have earned a return if they were invested, so the “opportunity cost” is even greater.

Instead, I invest in Vanguard’s FTSE Global All Cap Index Fund (Accumulation). This means I am invested in 100% equities (stocks), spread across the world’s publicly traded companies in proportion to their valuation, and any profits paid out (dividends) are automatically reinvested. This is a broad, diversified and passive fund, and means I am not trying to “beat the market” – I am just following it.

Because I’m far from retirement and my salary is my main source of income, I’m happy to take the added volatility and increased expected return that being fully invested in equities gives.

The main alternative – bonds, which is basically investing in loans to businesses and governments – tends to be less volatile, but give a smaller return. The chart above shows the performance of equities versus bonds between 1900 and 2017 – in my view, because I’m willing to live with the higher volatility and risk, 100% equities makes sense for me. (Ben Todd gives a counter-argument here, for what it’s worth.)

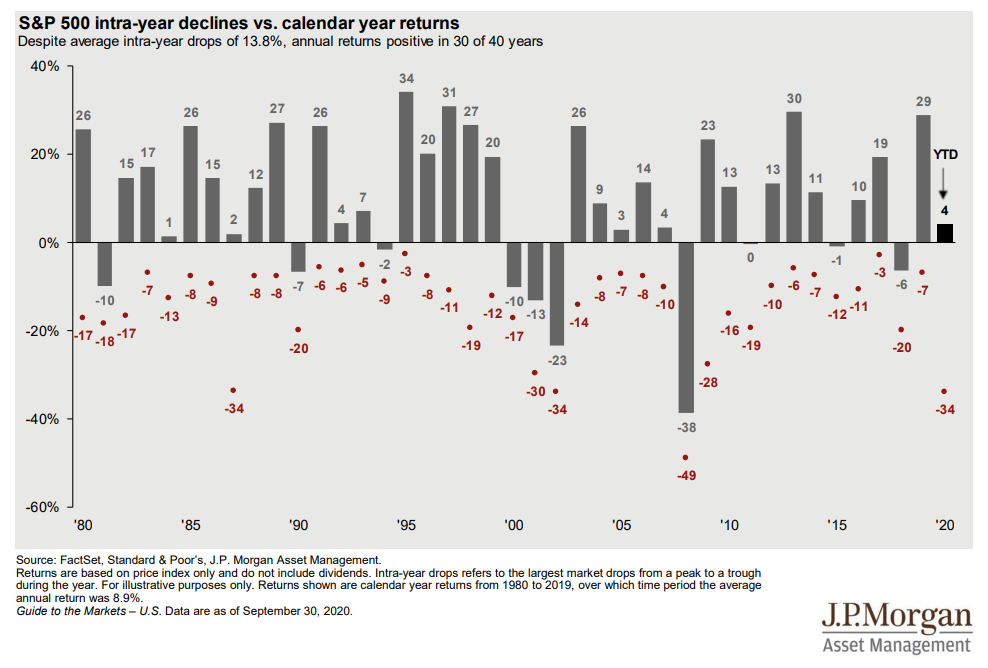

If you invest in equities, be prepared for some very unpleasant years, even though the average annual return may be positive. The chart above shows the S&P 500’s performance since 1980. I expect to live through a few major market drops, where I could lose as much as half of my savings or perhaps even more (the S&P 500, the main American stock tracker, lost 49% of its value in 2007-08). Even in good years I expect my savings to lose 20% of their value at some point, but I also expect that over the long term the extra returns will make those worth having lived through. I will probably move some of my savings into bonds as I get closer to retirement and am less able to “ride out” short-term drops in the market. Note: asset valuations are very high now, so don’t expect the same high returns we’ve had historically.

Vanguard’s Global All Cap Index Fund is the fund that I invest in. I own this share of the fund, and have chosen this instead of, eg, buying individual shares in Apple, the FTSE 100, or buying property. I pay a fee for this fund which pays the people who manage it. That fee is 0.23%, and is a charge on the total investment, not on the returns I make – so every year, I pay 0.23% of what I have invested, no matter how well or badly it performs. That means that what looks like a small fee can be very important: if you make a 1% return, a 0.23% fee eats nearly a quarter of your entire income from your investment. Thankfully, Vanguard’s 0.23% is very low compared to many other funds.

As well as choosing the fund I have also had to choose the platform to buy it on. If the fund is like the TV I buy, the platform is like the website I buy it from – Amazon, Currys, etc. Platforms also have their own fees.

I have chosen to use Vanguard’s platform, which costs another 0.15%, capped at £375 a year (meaning investments over £250,000 are effectively fee-free). So, in total, I pay 0.38% annually to invest. Other platforms are available, on which you can buy the fund I choose above and other funds on them too. (Confusingly, Vanguard is both a platform and has a range of funds.) There’s a comparison of platforms here.

These fees compare well with similar offerings from high street banks. Until recently, for example, Natwest charged a maximum of 0.35% in platform fees and 0.60% in fund fees for its stocks and shares ISA, making it over twice as expensive as my Vanguard choice. They’ve cut those fees a bit, so they’re now just under twice as expensive. Like I say, these fees might look small, but they’re best thought of as a percentage of your returns – if you expect to make 4% per year in real terms, a 0.95% total fee is a 24% charge on your returns, while a 0.38% fee is a 10% charge. Over the long term, this adds up.

I do all this through an ISA, which means that gains I make on these investments are not taxed. In the UK you can contribute up to £20,000 a year to your ISAs, which includes cash ISAs and ISAs for buying a house. Cash ISAs are pointless – you will not earn enough interest to pay tax on it – and I don’t plan on buying a house in the near future, so these are irrelevant to me.

I admit that I do “invest” a tiny amount of money in individual stocks, which I consider to be a form of gambling. I use Freetrade for this, which doesn’t have any fees for normal trading. I mostly own CRISPR-related stocks, but it’s less than 1% of my savings. Here’s a referral link to sign up – if you do, we’ll each get a “free share” worth about a fiver.

Managing my own pension

I self-manage my pension through a SIPP (Self-Invested Personal Pension). This is almost identical to the stocks and shares ISA I have above, and similarly is entirely in Vanguard’s FTSE Global All Cap Index Fund and invested on Vanguard’s site. It has the same fund and platform fees as Vanguard – some pensions have combined fees of 1% or higher, which over the lifetime of your pension can mean tens of thousands of pounds wasted.

Most pensions that people are opted into by their employers are either expensive and/or timid in how they invest. NEST is a public corporation in the UK that serves as the “default” pension fund for many employers. It was set up when autoenrollment was introduced, requiring workplaces to enroll their employees into a pension, and it has a range of different funds according to people’s expected retirement dates, risk tolerances, and ethical preferences. Since 2015, as spotted by Michael Lane, by far the best performing fund has been its Sharia fund:

So if you’d invested £100 in a NEST fund at the start of 2015, you would have about £170 if you’d gone for its Higher Risk Fund, and £246 if you’d gone for the Sharia fund, as of September 2020. You’d be even worse off if you’d gone with its default 2040 retirement fund!

This is because the Sharia fund is 100% equities, while the higher risk fund is only 70% equities and the default fund is 60% equities. Obviously, this reflects the excess risk that equities come with, but for me, this is not the sort of portfolio I want for a pension I will not be touching for another thirty years at least.

If I was in a normal pension, my first move would be to check the equity share of the investment and the pension fees, and compare them to alternatives. I have zero confidence in a pension fund manager’s ability to “beat the market” and so I do not believe in paying them to pick stocks for me. I want as diversified, passive and cheap a portfolio as possible, and a 100% equities investment to maximise long-term growth.

That’s not to say that employer pensions are bad: if your employer will match your contributions, that’s free money. When I had an employer that did that, I increased my contributions to get as much employer contribution as possible.

It’s pretty easy to move pensions – I moved two into Vanguard when I set up my SIPP. If I had an employer that refused to deal with my SIPP, I would maximise my contributions to their pension to get as much employer contribution as possible, and then move it out as soon as I’d moved to a new job.

NB: Pensions are not always good value in the first place, especially if you’re a basic rate taxpayer, because you get taxed on money you withdraw from them. Employer matching aside, if I was a basic rate taxpayer I would often prefer to contribute to my ISA (paying 20% on the way in, and then nothing on withdrawals) than to my pension (paying nothing on the way in, and 20% on withdrawals), because of the ability to access my ISA savings whenever I want, not just after I retire.

So, in summary: virtually all my long-term savings are held in equities in an all-world fund managed by Vanguard. I am focused on keeping my investments broad and cheap. I manage my own pension to do this too.

Why I don’t plan on buying a house

I am not planning on buying a house any time in the near future.

I don’t think it’s any cheaper than renting, when you account for the opportunity cost of investing the money you would have spent on the house. Buying a house involves both paying for the rent up front and investing in a house – I’d prefer to pay the rent on a monthly basis and invest my money elsewhere.

I think the transaction costs of buying and selling houses are enormous (stamp duty, the cost of finding a good place, and the risks involved with buying a house that has problems you don’t know about), so if I ever do buy a house I will want to do it as few times as possible.

I don’t expect to want to live in the same place when I have children as I do now that I don’t have any.

I am relatively optimistic and knowledgeable about the prospects of planning reform in the UK (which would lower the long-run expected path of house price rises), compared to the market as a whole, so I think in this I potentially can “beat the market” by waiting until my friends have succeeded in making houses cheaper.

I don’t think it’s stupid to buy a house that you expect to live in for a long time, because the benefits of being able to make it your own and put down roots somewhere without having a landlord who can force you to move might be significant. But it’s not for me right now. (I would probably never buy a flat, though, because you’re too much at risk of getting stuck with bad/noisy neighbours). There’s a good short podcast on the “buy or rent” debate here.

Budgeting with Monzo

Every month when I get paid, I use Monzo pots to divide my income between the following – the first three are each pots, separate from my main balance, and the fourth goes straight to Vanguard:

Rent and bills

Discretionary spending

Short-term savings

Long-term savings

Rent and bills don’t change month to month, so that’s easy – all of that comes out of a dedicated Monzo pot, so I just make sure to put the same amount in each month.

Then I put a month’s worth of other spending money into a “discretionary spending” pot – this includes all other day to day spending, including groceries and transport. Once a week, I move a week’s worth of spending from that pot into my main account. That is my total balance for the week and I can only add to it in exceptional circumstances. I do this on a Friday so I can have fun over the weekend and tighten my belt during the remaining weekdays – it’s a lot less miserable to be broke on a Wednesday than a Saturday.

I put a fixed amount into long-term savings, which I describe above – that goes into Vanguard. And then I put the rest into short-term savings, which is basically a slush fund for large and “long-term” expenses like holidays, clothes, electronics, etc. This also acts as my “emergency fund”, but as discussed above, this is very small – less than a month’s income, and equivalent to about a month’s expenses. If it gets too large, I put the excess into long-term savings.

This method means I am committing most of my money in advance, and replicates the “envelope method” to portion out spending across a month. The only flaw in this is if there is a special event I’m going to, like a birthday party, where I’ll end up spending more in a given week than usual. In those cases, I usually take from my short-term savings slush fund.

Summary

I try to apportion my money fairly rigidly each month for short-term budgeting. I keep a small amount of short-term savings in cash, and I invest virtually all the rest in a low-cost index fund. I hope this has helped you think about what may be best for your money – don’t just follow what I do, but look into it yourself. It’s daunting but it’s actually not very complex, and you could make yourself much better off in the long run than if you just sit on cash or whatever default investment fund or pension your bank or employer has given you.

Thanks to friends who helped me with this, especially Michael Lane.